Let me ask you something that most people avoid thinking about.

If you weren’t here tomorrow — really, truly gone — would the people you love most be financially okay?

Not emotionally okay. That’s a different conversation. But financially — could they pay the mortgage? Cover the kids’ school tuition? Handle the medical bills, the funeral costs, and still keep the lights on six months from now?

For millions of American families, the honest answer is no.

And the painful part? It didn’t have to be that way.

Life insurance is one of those things people know they need but somehow never get around to buying. It sits on the mental to-do list right next to “start saving for retirement” and “actually eat healthier.” But unlike a gym membership, skipping life insurance doesn’t just hurt you — it can financially devastate the people you care about most.

This guide cuts through all the noise. No insurance jargon. No pushy sales tactics. Just a clear, research-backed, honest look at the best life insurance companies and policies in 2026 — so you can make a smart, confident decision today.

📊 Why Life Insurance Is More Critical Than Ever in 2026

The numbers tell a sobering story.

According to LIMRA’s 2025 Insurance Barometer Report — one of the most comprehensive annual studies on life insurance in the United States — 51% of Americans say they need more life insurance than they currently have, and approximately 100 million Americans remain uninsured or underinsured as of late 2025.

(Source: LIMRA 2025 Insurance Barometer Study)

Meanwhile, the financial stakes have never been higher:

- 🏠 Average U.S. mortgage balance: $244,498 (Source: Federal Reserve Bank of New York, Q3 2025)

- 💀 Average funeral and burial cost in 2025: $8,300–$12,000 (Source: National Funeral Directors Association, 2025)

- 🎓 Average annual cost of a 4-year public university: $27,146 per year (Source: College Board, Trends in College Pricing 2025)

- 💳 Average American household debt: $104,215 (Source: Experian State of Credit Report, 2025)

These aren’t just statistics. They represent real financial pressure that falls directly on your family’s shoulders the moment you’re gone — unless you’ve planned ahead.

And here’s the kicker: life insurance is more accessible and affordable than most people think.

A healthy 30-year-old non-smoker can get a $500,000 20-year term life insurance policy for as little as $18–$25 per month in 2026. That’s less than most people spend on streaming subscriptions.

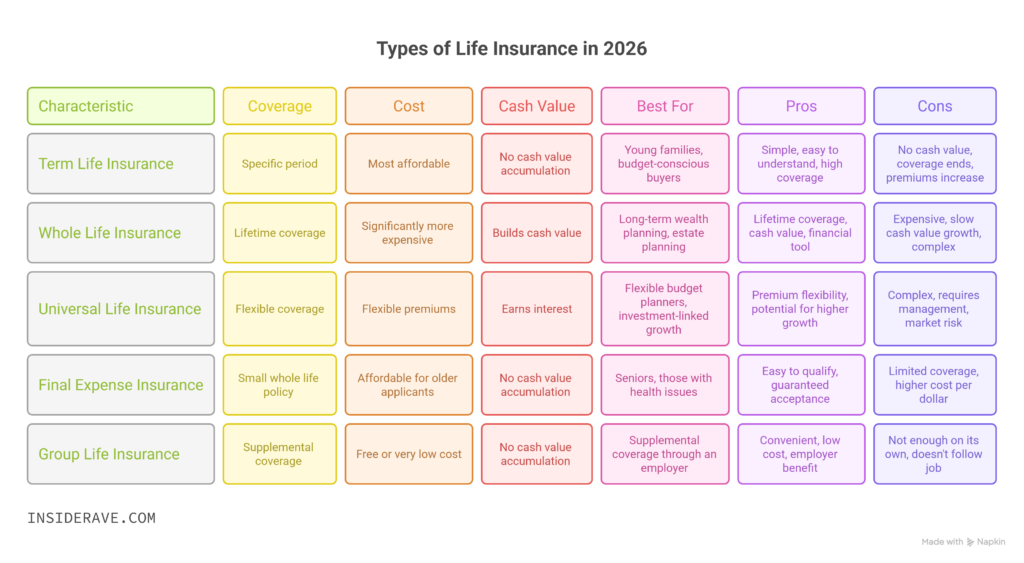

🔍 Understanding the Types of Life Insurance in 2026

Before you compare companies, you need to know what you’re actually shopping for. The “best” policy isn’t universal — it depends entirely on your age, budget, health, and financial goals.

Here’s a straightforward breakdown:

1. Term Life Insurance

Best for: Young families, budget-conscious buyers, income replacement

Term life covers you for a specific period — typically 10, 15, 20, or 30 years. If you pass away during the term, your beneficiaries receive the death benefit. If the term expires, the coverage ends (though many policies offer renewal or conversion options).

Pros:

- Most affordable type of life insurance

- Simple and easy to understand

- High coverage amounts at low premiums

Cons:

- No cash value accumulation

- Coverage ends when the term expires

- Premiums increase significantly if you renew at an older age

💡 2026 Insight: Term life insurance remains the most purchased type of individual life insurance in the USA, accounting for over 71% of new policy sales in 2024–2025. (Source: LIMRA U.S. Life Insurance Sales Report, 2025)

2. Whole Life Insurance

Best for: Long-term wealth planning, estate planning, lifelong coverage needs

Whole life insurance is permanent coverage — it never expires as long as you pay your premiums. It also builds cash value over time, which you can borrow against or withdraw.

Pros:

- Lifetime coverage guaranteed

- Cash value grows at a fixed rate (typically 1.5%–3% annually)

- Can serve as a financial planning tool

Cons:

- Significantly more expensive than term (often 5–15x higher premiums)

- Cash value growth is slower compared to investing independently

- Complex product with many variations

3. Universal Life Insurance

Best for: Flexible budget planners, those wanting investment-linked growth

Universal life is a form of permanent insurance with flexible premiums and death benefits. The cash value earns interest based on market rates or indexes (in the case of Indexed Universal Life, or IUL).

Pros:

- Premium flexibility

- Potential for higher cash value growth

- Adjustable death benefit

Cons:

- More complex than term or whole life

- Requires active management

- Market-linked versions carry risk

4. Final Expense Insurance

Best for: Seniors, those with health issues, covering burial costs only

Final expense (also called burial insurance) is a small whole life policy designed to cover end-of-life costs. Coverage typically ranges from $5,000 to $25,000.

Pros:

- Easy to qualify for (often no medical exam)

- Guaranteed acceptance options available

- Affordable for older applicants

Cons:

- Limited coverage amounts

- Higher cost per dollar of coverage compared to term

5. Group Life Insurance

Best for: Supplemental coverage through an employer

Many American employers offer group life insurance as part of their benefits package — typically 1–2x your annual salary. It’s convenient and often free or very low cost, but it’s rarely enough on its own and doesn’t follow you if you change jobs.

⚠️ Important: Financial experts recommend using employer-provided group coverage as a supplement, not a replacement, for individual life insurance.

🏆 Best Life Insurance Companies in 2026: Detailed Rankings

After analyzing financial strength ratings, customer satisfaction scores, policy options, pricing transparency, claims processing speed, and digital experience, here are the top life insurance companies in 2026 for American consumers.

🥇 1. Northwestern Mutual — Best Overall

Why it stands out: Northwestern Mutual has maintained an AM Best A++ (Superior) rating for decades — the highest possible rating. It consistently ranks at the top for financial stability, dividend performance, and customer trust.

- Policy types: Term, Whole, Universal, Variable Universal

- AM Best Rating: A++ (Source: AM Best, 2025)

- J.D. Power Customer Satisfaction: 790/1,000 (above industry average) (Source: J.D. Power 2025 U.S. Individual Life Insurance Study)

- Coverage amounts: $100,000 to $10M+

- Best for: High-income earners, long-term financial planners, whole life buyers

🔗 (Source: AM Best Northwestern Mutual Rating | J.D. Power 2025 Life Insurance Study)

🥈 2. Haven Life (Backed by MassMutual) — Best for Affordable Term Life Online

Why it stands out: Haven Life is a 100% online term life insurance provider backed by MassMutual (rated A++ by AM Best). It’s designed for the modern buyer who wants fast, transparent, no-hassle term coverage.

- Policy types: Term Life (InstaTerm and Term with medical exam)

- AM Best Rating: A++ (MassMutual backing)

- Instant approval: Available for eligible applicants up to age 59

- Coverage amounts: $100,000 to $3M

- Starting cost: ~$15–$20/month for healthy 30-year-olds

- Best for: Tech-savvy buyers, young professionals, those wanting fast coverage

🥉 3. State Farm — Best for Customer Service & Local Agent Support

Why it stands out: State Farm has been a household name in American insurance for over 100 years. It earns top marks year after year for claims satisfaction and agent accessibility.

- Policy types: Term, Whole, Universal

- AM Best Rating: A++ (Source: AM Best, 2025)

- J.D. Power Customer Satisfaction: 843/1,000 — #1 ranked in J.D. Power 2025 (Source: J.D. Power 2025 U.S. Individual Life Insurance Study)

- Coverage amounts: $100,000 to $10M+

- Best for: Families who want face-to-face agent support, bundling with home/auto insurance

4. New York Life — Best Whole Life Insurance

Why it stands out: Founded in 1845, New York Life is one of the oldest and most financially stable insurance companies in America. It’s a mutual company, meaning policyholders share in profits through dividends.

- Policy types: Term, Whole, Universal, Variable Universal

- AM Best Rating: A++ (Source: AM Best, 2025)

- Dividend history: Has paid dividends to whole life policyholders every year since 1854 (Source: New York Life)

- Best for: Whole life buyers, estate planning, high-net-worth individuals

5. Protective Life — Best for Low-Cost Term Life

Why it stands out: Protective Life consistently offers some of the lowest term life rates in the USA market, particularly for 30-year term policies. A strong choice for budget-conscious buyers who want maximum coverage.

- Policy types: Term, Whole, Universal, Variable Universal

- AM Best Rating: A+ (Source: AM Best, 2025)

- Term lengths: 10, 15, 20, 25, 30, 35, 40 years (one of the longest terms available)

- Starting cost: ~$14–$18/month for healthy applicants

- Best for: Those wanting the longest possible term coverage at the lowest price

6. Mutual of Omaha — Best Final Expense & Senior Coverage

Why it stands out: Mutual of Omaha is the go-to provider for final expense insurance and senior life coverage in the USA. Their guaranteed issue whole life policy requires no medical exam and no health questions.

- Policy types: Term, Whole, Final Expense, Guaranteed Issue

- AM Best Rating: A+ (Source: AM Best, 2025)

- J.D. Power Score: 779/1,000 (Source: J.D. Power 2025)

- Coverage amounts: $2,000–$25,000 (final expense) | Up to $1M (term)

- Best for: Seniors aged 45–85, those with pre-existing conditions, burial coverage

7. USAA — Best for Military Families

Why it stands out: USAA is exclusively available to military members, veterans, and their families — and for that community, it’s simply the gold standard. Exceptional pricing, extraordinary customer service, and military-specific benefits make it unmatched in its niche.

- Policy types: Term, Whole, Universal

- AM Best Rating: A++ (Source: AM Best, 2025)

- J.D. Power Customer Satisfaction: 893/1,000 — consistently among the highest scores (Source: J.D. Power 2025)

- Best for: Active military, veterans, military spouses and dependents

8. Ethos Life — Best for Fast No-Exam Coverage

Why it stands out: Ethos uses AI-powered underwriting to offer near-instant life insurance decisions without a medical exam for most applicants. Coverage can be active in as little as 10 minutes.

- Policy types: Term, Guaranteed Whole Life

- Underwriting partners: Multiple A-rated carriers

- Coverage amounts: $20,000–$2M

- Starting cost: ~$14/month

- Best for: Applicants who want fast coverage, those who dislike medical exams, older applicants seeking guaranteed issue

📊 Quick Comparison Table: Best Life Insurance Companies 2026

| Company | Best For | Policy Types | AM Best Rating | J.D. Power Score | Est. Monthly Cost* |

|---|---|---|---|---|---|

| Northwestern Mutual | Overall Best | Term, Whole, Universal | A++ | 790/1,000 | ~$25+ |

| Haven Life | Online Term | Term | A++ (MassMutual) | N/A | ~$15–$20 |

| State Farm | Customer Service | Term, Whole, Universal | A++ | 843/1,000 | ~$22–$28 |

| New York Life | Whole Life | Term, Whole, Universal | A++ | 774/1,000 | ~$30+ |

| Protective Life | Low-Cost Term | Term, Whole, Universal | A+ | 757/1,000 | ~$14–$18 |

| Mutual of Omaha | Seniors/Final Expense | Term, Whole, Final Expense | A+ | 779/1,000 | ~$20–$30 |

| USAA | Military Families | Term, Whole, Universal | A++ | 893/1,000 | ~$18–$25 |

| Ethos Life | No-Exam Fast Coverage | Term, Whole | A-rated carriers | N/A | ~$14–$22 |

Estimated monthly costs are for a healthy non-smoking 30-year-old with $500,000 in 20-year term coverage. Actual rates vary based on age, health, gender, state, and coverage amount.

💡 How to Choose the Right Life Insurance Policy in 2026

Shopping for life insurance doesn’t have to feel like solving a puzzle. Here’s a step-by-step framework that financial advisors actually recommend:

Step 1: Calculate Your Real Coverage Need

The old “10x your salary” rule is a starting point — but it’s outdated for many Americans. A more precise method is the DIME formula:

- D — Debts (all debts outside of mortgage)

- I — Income (years until retirement × annual income)

- M — Mortgage (outstanding balance)

- E — Education (estimated cost for each child’s education)

Example: If you earn $75,000/year, have 25 years until retirement, a $250,000 mortgage, $30,000 in other debts, and two children needing $100,000 each for college — your coverage need = $2,255,000.

Step 2: Choose Your Policy Type

| Your Situation | Recommended Policy |

|---|---|

| Young family on a budget | 20–30 year term |

| Lifelong coverage + estate planning | Whole life |

| Flexible premium budget | Universal life |

| Senior needing burial coverage | Final expense |

| Military member or veteran | USAA term or whole |

Step 3: Compare Quotes from Multiple Providers

Never buy the first quote you receive. Use these trusted comparison platforms:

- Policygenius — Best overall comparison tool (policygenius.com)

- NerdWallet Life Insurance — Great for unbiased reviews (nerdwallet.com)

- SelectQuote — Works with 15+ top carriers (selectquote.com)

- Ladder Life — Best for adjustable term coverage (ladderlife.com)

Step 4: Verify Financial Strength

Always check the insurer’s AM Best financial strength rating before buying. Here’s what the ratings mean:

| AM Best Rating | What It Means |

|---|---|

| A++ | Superior financial strength |

| A+ | Superior financial strength |

| A | Excellent financial strength |

| A- | Excellent financial strength |

| B++ | Good — acceptable but monitor |

| Below B++ | Caution — consider alternatives |

🔗 (Source: AM Best Rating Scale)

Step 5: Understand Key Policy Riders

Riders are add-ons that customize your policy. Some of the most valuable include:

- Waiver of Premium Rider — Waives your premium if you become disabled

- Accelerated Death Benefit Rider — Access part of your death benefit if diagnosed with terminal illness

- Child Term Rider — Adds coverage for your children at low cost

- Convertibility Rider — Allows you to convert term to permanent without a new medical exam

- Return of Premium Rider — Returns all premiums paid if you outlive the term (costs more but appeals to many)

⚠️ Common Life Insurance Mistakes Americans Make in 2026

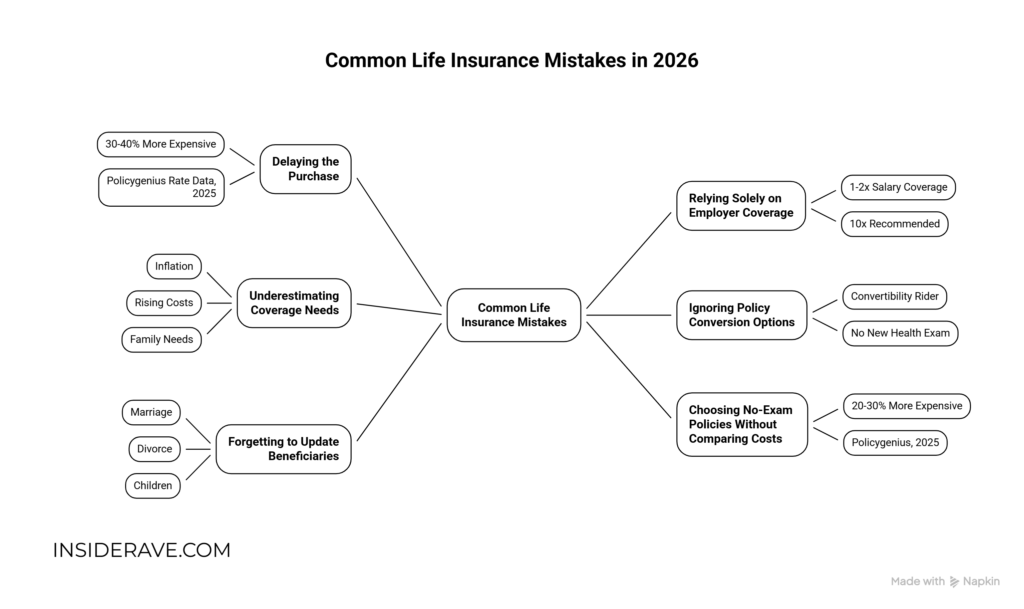

Learning from others’ mistakes can save you thousands of dollars and protect your family more effectively.

- ❌ Delaying the purchase — Every year you wait, premiums increase. A 35-year-old pays roughly 30–40% more than a 28-year-old for the same coverage. (Source: Policygenius Rate Data, 2025)

- ❌ Relying solely on employer coverage — Group life insurance typically covers only 1–2x your salary. Most financial experts recommend a minimum of 10x.

- ❌ Underestimating coverage needs — Inflation, rising costs of living, and growing family needs mean many people are significantly underinsured.

- ❌ Ignoring policy conversion options — If your term policy has a convertibility rider, you can switch to permanent coverage without a new health exam — valuable if your health declines.

- ❌ Forgetting to update beneficiaries — After major life events (marriage, divorce, having children), update your beneficiaries immediately.

- ❌ Choosing no-exam policies without comparing costs — No-exam policies typically cost 20–30% more than fully underwritten policies. (Source: Policygenius, 2025)

💰 Life Insurance Rates in 2026: What to Expect

Here’s a detailed rate comparison for a $500,000 20-year term life policy based on age and gender for healthy non-smokers:

| Age | Male (Monthly) | Female (Monthly) |

|---|---|---|

| 25 | ~$18 | ~$15 |

| 30 | ~$22 | ~$18 |

| 35 | ~$28 | ~$23 |

| 40 | ~$42 | ~$35 |

| 45 | ~$68 | ~$55 |

| 50 | ~$110 | ~$85 |

| 55 | ~$175 | ~$130 |

Estimates based on aggregate rate data from Policygenius, SelectQuote, and Protective Life (2025). Actual rates vary by carrier, health classification, state, and specific underwriting criteria.

📌 Key takeaway: Buying at age 30 versus 40 saves the average American male approximately $240 per year — or $4,800 over a 20-year term. Don’t wait.

❓ Frequently Asked Questions (FAQs)

Q1: How much life insurance do I actually need in 2026?

Most financial advisors recommend coverage of 10–15 times your annual income, but using the DIME formula (Debts + Income replacement + Mortgage + Education) gives you a more precise number tailored to your family’s real financial needs.

Q2: What is the best life insurance company in the USA in 2026?

Based on financial strength, customer satisfaction, and policy options, Northwestern Mutual, State Farm, and Haven Life consistently rank among the best in 2026. The “best” company depends on your specific needs — term vs. whole life, budget, and health profile.

Q3: Can I get life insurance with pre-existing conditions?

Yes. Many companies offer guaranteed issue or simplified issue policies that don’t require a medical exam. Expect higher premiums, but coverage is absolutely obtainable. Mutual of Omaha and Ethos Life are strong options for those with health concerns.

Q4: Is term or whole life insurance better in 2026?

For most Americans — especially those under 45 with dependents — term life insurance offers the best value. It provides high coverage at low cost during your most financially vulnerable years. Whole life makes more sense for estate planning, business succession, or lifelong coverage needs.

Q5: How long does it take to get approved for life insurance?

- No-exam policies (Ethos, Haven Life): As fast as 10 minutes to 48 hours

- Simplified underwriting: 1–3 weeks

- Fully underwritten policies: 4–8 weeks (involves medical exam and labs)

Q6: Is life insurance taxable in the USA?

In most cases, life insurance death benefits are income-tax-free for beneficiaries under IRS rules. However, interest earned on death benefits, certain business-owned policies, and cash value withdrawals may have tax implications. Always consult a tax advisor for your specific situation. (Source: IRS Publication 525)

Q7: What happens if I outlive my term life insurance policy?

If you outlive your term policy, coverage simply ends. You have several options: renew the policy (at significantly higher rates), convert to a permanent policy (if your policy includes a conversion rider), or purchase a new policy. Many people find they need less coverage by the time their term expires — mortgage is paid down, kids are grown, and savings have accumulated.

🎯 Final Thoughts: The Best Time to Buy Life Insurance Is Right Now

Here’s the honest truth about life insurance that nobody really wants to hear:

The best policy is the one you actually have.

Not the one you’re researching forever. Not the one you’ll get around to “someday.” The one that’s active right now, protecting your family against the unexpected.

Yes, comparing quotes matters. Yes, choosing a financially strong company matters. But overthinking this decision while months and years pass? That’s the most expensive mistake of all.

Your family deserves protection. You deserve the peace of mind that comes from knowing they’ll be okay no matter what happens.

So take that one step today. Get a quote. Compare a few options. Talk to a licensed agent if you need guidance. And stop letting “someday” be the plan.

Because love isn’t just something you feel. It’s something you plan for.

🌐 Suggested External Authority Sources

| Source | URL |

|---|---|

| LIMRA 2025 Insurance Barometer Study | limra.com |

| AM Best Financial Strength Ratings | ambest.com |

| J.D. Power 2025 Life Insurance Study | jdpower.com |

| National Funeral Directors Association | nfda.org |

| College Board Trends in College Pricing | collegeboard.org |

| Experian State of Credit Report 2025 | experian.com |

| IRS Publication 525 (Taxable Income) | irs.gov |

| Policygenius Life Insurance Marketplace | policygenius.com |

| Federal Reserve Bank of New York | newyorkfed.org |

📌 Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, legal, or insurance advice. Data and statistics are sourced from publicly available reports as of 2025–2026. Always consult a licensed insurance professional before purchasing any policy. Policy availability, pricing, and features vary by state and individual circumstances.