Picture this.

Two neighbors — let’s call them Marcus and Derek — both 32 years old, both married with young kids, both making around $80,000 a year. Both finally decide to stop procrastinating and buy life insurance in 2026.

Marcus goes with a 20-year term life policy at $500,000 coverage. His monthly premium? $23.

Derek, after talking to a different agent, signs up for a whole life insurance policy with a $500,000 death benefit. His monthly premium? $412.

Same age. Same coverage amount. Nearly 18 times the price difference.

So who made the right call?

That’s exactly the question this guide answers — honestly, thoroughly, and without the insurance industry spin. Because the truth is, neither policy is universally “better.” The right answer depends entirely on your financial situation, your goals, your family’s needs, and how you think about money.

Let’s break it all down.

📊 The State of Life Insurance in 2026: Where Americans Stand

Before diving into the comparison, it helps to understand the landscape.

According to LIMRA’s 2025 Insurance Barometer Study, term life insurance accounts for approximately 71% of all individual life insurance policies sold in the United States — making it by far the most popular choice among American consumers.

(Source: LIMRA 2025 Insurance Barometer Study)

Yet whole life insurance continues to grow steadily, particularly among:

- High-income earners using it as a wealth-building tool

- Business owners leveraging it for succession planning

- Parents funding permanent legacy strategies for their children

(Source: Insurance Information Institute, Life Insurance Facts & Stats 2025)

Meanwhile, 41% of Americans say cost is the #1 barrier to purchasing life insurance — which is precisely why understanding the real price difference between these two products matters so much.

(Source: LIMRA 2025 Insurance Barometer Study)

🔍 What Is Term Life Insurance? A Clear, Simple Explanation

Term life insurance does exactly what its name suggests. It covers you for a specific term — typically 10, 15, 20, or 30 years. If you die within that term, your beneficiaries receive the death benefit. If you outlive the policy, coverage ends.

That’s it. No investment component. No cash value. Just pure, straightforward death benefit protection.

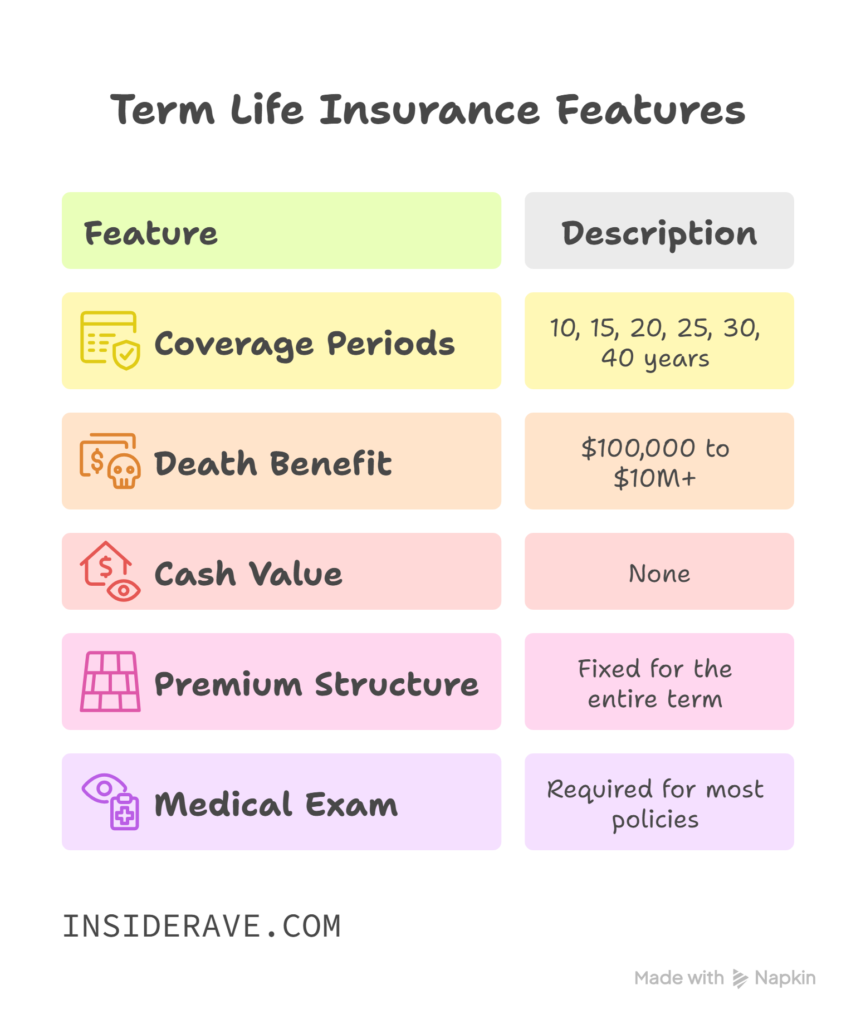

Key Features of Term Life Insurance:

- Coverage periods: 10, 15, 20, 25, 30, and even 40-year terms available in 2026

- Death benefit: $100,000 to $10M+ depending on the carrier

- Cash value: None

- Premium structure: Fixed for the entire term (level term)

- Medical exam: Required for most fully underwritten policies; optional for no-exam versions

Who Typically Buys Term Life?

- Young parents who need income replacement protection

- Homeowners wanting to cover their mortgage balance

- Couples with significant debt (student loans, car loans, credit cards)

- Anyone who needs maximum coverage at minimum cost

🔍 What Is Whole Life Insurance? The Full Picture

Whole life insurance is a form of permanent life insurance — meaning it doesn’t expire. As long as you pay your premiums, your beneficiaries are guaranteed a death benefit whenever you pass away, whether that’s at age 45 or 95.

But here’s what makes whole life fundamentally different from term: it includes a cash value component that grows over time at a guaranteed rate — typically between 1.5% and 4% annually, depending on the carrier and dividend performance.

(Source: New York Life Whole Life Policy Disclosures, 2025)

That cash value is a living benefit — you can borrow against it, use it to pay premiums, or even surrender the policy for its accumulated value.

Key Features of Whole Life Insurance:

- Coverage period: Lifetime (permanent)

- Death benefit: Guaranteed, often with potential to grow via dividends

- Cash value: Yes — grows at a fixed, guaranteed rate

- Premium structure: Fixed for life, significantly higher than term

- Dividends: Participating policies (like those from Northwestern Mutual and New York Life) may pay annual dividends

Who Typically Buys Whole Life?

- High-income individuals looking for tax-advantaged wealth accumulation

- Business owners using it for key person insurance or buy-sell agreements

- Parents wanting to fund a child’s future financial needs

- Those with estate planning goals and permanent coverage needs

- Individuals with lifelong dependents (special needs family members, for example)

⚖️ Term vs. Whole Life Insurance: Head-to-Head Comparison

Let’s put both policies side by side across the metrics that matter most to American consumers in 2026:

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | Fixed term (10–40 years) | Lifetime (permanent) |

| Monthly Premium (30yo, $500K) | ~$22–$28 | ~$400–$500 |

| Cash Value | None | Yes — grows over time |

| Death Benefit | Fixed | Fixed + potential dividend growth |

| Flexibility | Low (set term) | Moderate (loan options) |

| Investment Component | No | Yes (guaranteed growth) |

| Complexity | Simple | Complex |

| Best For | Income replacement, debt coverage | Wealth transfer, estate planning |

| Tax Advantages | Death benefit is tax-free | Cash value grows tax-deferred |

| Surrender Value | None | Yes (after sufficient time) |

| AM Best Carrier Options | Abundant | Abundant |

| Convertibility | Often convertible to whole life | N/A |

Rate estimates based on aggregate data from Policygenius, SelectQuote, and Protective Life (2025) for healthy, non-smoking 30-year-old males.

💰 The Real Cost Difference: Where the Numbers Get Eye-Opening

Let’s go deeper on the cost comparison, because this is where most people make or break their decision.

Term Life: Sample Monthly Rates in 2026

$500,000 / 20-Year Term / Healthy Non-Smoker:

| Age | Male | Female |

|---|---|---|

| 25 | ~$18/mo | ~$15/mo |

| 30 | ~$22/mo | ~$18/mo |

| 35 | ~$28/mo | ~$23/mo |

| 40 | ~$42/mo | ~$35/mo |

| 45 | ~$68/mo | ~$55/mo |

| 50 | ~$110/mo | ~$85/mo |

(Source: Policygenius Rate Data, SelectQuote Estimates, 2025)

Whole Life: Sample Monthly Rates in 2026

$500,000 / Whole Life / Healthy Non-Smoker:

| Age | Male | Female |

|---|---|---|

| 25 | ~$350/mo | ~$300/mo |

| 30 | ~$420/mo | ~$360/mo |

| 35 | ~$510/mo | ~$430/mo |

| 40 | ~$640/mo | ~$540/mo |

| 45 | ~$820/mo | ~$690/mo |

| 50 | ~$1,050/mo | ~$880/mo |

(Source: New York Life, Northwestern Mutual public rate estimates, 2025)

The “Buy Term and Invest the Difference” Argument

One of the most debated concepts in personal finance is whether you should buy term and invest the difference in premiums rather than pay whole life premiums.

Here’s how the math works using Marcus and Derek from our opening example:

- Derek pays $412/month for whole life

- Marcus pays $23/month for term

- Difference: $389/month

If Marcus invested that $389/month difference in a low-cost S&P 500 index fund averaging 10% annual returns (the historical average since 1957), over 20 years he would accumulate approximately:

~$267,000 in invested assets — completely separate from his $500,000 life insurance death benefit.

(Source: S&P 500 historical return data via Investopedia)

However — and this is critical — this comparison only works if Marcus actually disciplines himself to invest that difference consistently. Many people don’t. And whole life’s forced savings component has real psychological value for those who struggle with investing discipline.

✅ When Term Life Insurance Is the Right Choice

Term life insurance is almost certainly the better choice if:

- ✔️ You’re under 45 with dependents who rely on your income

- ✔️ You have a mortgage you want covered if you pass away

- ✔️ Your primary goal is income replacement for a defined period

- ✔️ You’re on a tight budget and need maximum coverage affordably

- ✔️ You’re self-disciplined enough to invest the premium difference

- ✔️ You want simplicity without complex financial products

- ✔️ Your need for coverage has a defined end date (when kids grow up, mortgage is paid off, retirement savings are sufficient)

💡 Expert Consensus: The vast majority of certified financial planners (CFPs) recommend term life insurance for most middle-income American families as the most efficient use of insurance dollars.

(Source: CFP Board Consumer Resources, 2025)

✅ When Whole Life Insurance Is the Right Choice

Whole life insurance makes genuine financial sense if:

- ✔️ You have lifelong dependents (a child with special needs, for example) who will always need financial protection

- ✔️ You’ve maxed out all other tax-advantaged accounts (401k, IRA, HSA) and need additional tax-deferred growth

- ✔️ You have a high net worth and want to minimize estate taxes through life insurance strategies

- ✔️ You’re a business owner using life insurance for key person coverage or buy-sell agreement funding

- ✔️ You want a guaranteed death benefit regardless of how long you live

- ✔️ You value the forced savings discipline that whole life provides

- ✔️ You’re purchasing for a young child to lock in low rates and build long-term cash value

🤔 The Hybrid Approach: Can You Have Both?

Absolutely — and many financially savvy Americans do exactly this.

A common strategy is to:

- Purchase a large term life policy for primary income replacement protection

- Add a smaller whole life policy for permanent coverage, estate planning, or cash value accumulation

This gives you the affordability of term for your peak coverage years while maintaining permanent protection for specific long-term goals.

Another increasingly popular option in 2026 is convertible term life insurance — a term policy with a rider allowing you to convert part or all of your coverage to a whole life or universal life policy later, without a new medical exam.

This is especially valuable if your health declines before your term expires.

🧠 What Financial Experts and Advisors Say in 2026

The professional consensus in 2026 leans clearly toward term life for most Americans — but with important nuance:

“For the average American family earning under $150,000 annually, term life insurance provides the most efficient death benefit protection. Whole life has legitimate uses, but they’re specific and situational — not universal.”

— Certified Financial Planner, Fee-Only Advisor perspective (Source: NAPFA Consumer Resources, 2025)

“The appeal of whole life insurance is real for certain clients — particularly those in estate planning situations or those who have maximized traditional retirement vehicles. But it should never be sold as a one-size-fits-all solution.”

— Insurance industry analysis (Source: Insurance Information Institute, 2025)

⚠️ Red Flags to Watch For When Shopping in 2026

Whether you’re leaning toward term or whole life, watch out for these warning signs:

- 🚩 Agents pushing whole life on young, middle-income buyers — It’s often commission-driven. Whole life commissions are significantly higher than term.

- 🚩 “Overfunded” whole life pitches — Be skeptical of agents marketing whole life primarily as an investment vehicle.

- 🚩 Misleading “infinite banking” schemes — While some whole life strategies are legitimate, many marketed as “infinite banking” are oversimplified or unsuitable for most buyers.

- 🚩 Pressure to decide immediately — Reputable agents give you time to compare and consult independently.

- 🚩 No discussion of your specific financial situation — A good agent asks questions before recommending any product.

🎯 So — Term or Whole Life? Here’s Your Simple Decision Guide

Choose Term Life if:

You need affordable, high-coverage protection during your working and child-rearing years. You’re focused on income replacement and debt coverage. Budget matters.

Choose Whole Life if:

You have permanent coverage needs, estate planning goals, have maxed other retirement accounts, or are a high-net-worth individual seeking tax-advantaged wealth transfer.

Consider Both if:

You want layered coverage — term for primary protection now, permanent coverage for specific long-term goals.

❓ Frequently Asked Questions (FAQs)

Q1: Is term life insurance better than whole life for most Americans?

For the majority of middle-income American families, yes. Term life provides maximum coverage at minimum cost during the years when financial protection matters most. Whole life serves specific, more complex financial needs.

Q2: Can I switch from term to whole life insurance later?

Yes — if your term policy includes a convertibility rider, you can convert to a permanent policy without a new medical exam. This is one of the most valuable features to look for when purchasing term life in 2026.

Q3: Does whole life insurance pay dividends?

Some whole life policies — called participating policies — pay annual dividends when the insurer performs well financially. Companies like Northwestern Mutual and New York Life have paid dividends consistently for over 100 years. However, dividends are not guaranteed.

(Source: Northwestern Mutual, New York Life public disclosures, 2025)

Q4: What happens to term life insurance if I outlive my policy?

Coverage simply ends. You can typically renew (at much higher rates), convert to permanent coverage, or purchase a new policy. Many people find they need significantly less coverage by the time their term expires.

Q5: Is the cash value in whole life insurance taxable?

Cash value in whole life insurance grows tax-deferred, meaning you don’t pay taxes on the growth each year. Policy loans against cash value are generally tax-free. However, surrendering a policy for more than you paid in premiums may trigger tax liability. Always consult a tax advisor.

(Source: IRS Publication 525)

Q6: How much term life insurance do I need in 2026?

Most financial experts recommend 10–15 times your annual income, though the DIME formula (Debts + Income replacement + Mortgage + Education costs) provides a more personalized and accurate estimate for your specific family situation.

Q7: At what age does term life insurance stop making sense?

There’s no universal cutoff, but as you age into your late 50s and 60s, term premiums rise significantly. At that stage, if you have sufficient retirement savings, a paid-off mortgage, and grown children, your need for large-scale life insurance protection may have naturally decreased.

📝 Final Thoughts: The Right Policy Is the One Built Around Your Life

Marcus and Derek from the beginning of this article? Both actually made reasonable decisions — for their own situations.

Marcus, with young kids, a mortgage, and a tight monthly budget, got exactly what his family needed — half a million dollars of protection for the price of a Netflix subscription and a dinner out.

Derek, a business owner with estate planning needs and a maxed-out 401(k), found genuine value in the permanent coverage, cash value growth, and long-term wealth transfer that whole life provided.

The lesson isn’t that one is right and one is wrong. The lesson is that life insurance isn’t one-size-fits-all — and anyone who tells you it is, without asking about your specific situation first, isn’t serving your best interests.

Know your goals. Calculate your real needs. Compare multiple quotes. And buy the policy that actually fits your life — not someone else’s sales pitch.

Your family’s financial future is worth getting this right.

🌐 Suggested External Authority Sources

| Source | URL |

|---|---|

| LIMRA 2025 Insurance Barometer Study | limra.com |

| Insurance Information Institute | iii.org |

| AM Best Financial Strength Ratings | ambest.com |

| CFP Board Consumer Resources | cfp.net |

| NAPFA (Fee-Only Financial Advisors) | napfa.org |

| IRS Publication 525 | irs.gov |

| Investopedia S&P 500 Historical Returns | investopedia.com |

| Policygenius Life Insurance Marketplace | policygenius.com |

| New York Life Policy Disclosures | newyorklife.com |

| Northwestern Mutual Research | northwesternmutual.com |

📌 Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial, legal, or insurance advice. All rate estimates are approximations based on publicly available data from 2025–2026. Individual premiums vary based on age, health, gender, state of residence, and insurer underwriting criteria. Always consult a licensed insurance professional and/or certified financial planner before purchasing any life insurance policy.